The Big Payback

Last week, my student loan debt, a total of nearly $55,000, was entirely forgiven. All of it. Gone. Poof. Good riddance. Buh-bye.

Although the timing of my loan forgiveness aligns nicely with President Biden’s cancellation of up to $10,000 in federal student debt for Americans earning less than $125,000 per year, my own loan forgiveness has absolutely nothing to do with his historic announcement. Rather, my forgiveness is due entirely to the Public Service Loan Forgiveness (PSLF) temporary waiver the same president put into effect in October 2021.

Now, before I unpack the seemingly endless nonsense related to student loans (and I do – this is a LONG blog), I want to start by explaining, on behalf of the people for whom my same kind of loan forgiveness may apply, how both the program and the temporary waiver work so you too can benefit from this literal once-in-a-lifetime opportunity. Because nearly a year after its announcement and with only one month still left to apply, only 15 percent of the nine million public service workers with student loan debt have filed paperwork to determine their eligibility for the PSLF waiver. So please, if the following applies to you, get on it, and do it now because the waiver expires on Oct. 31, 2022. I did, and here I am, drinking champagne, with a big ass $55,000 weight off my shoulders.

Public Service Loan Forgiveness Overview

The PSLF Program was created under the College Cost Reduction and Access Act in 2007 during President George W. Bush’s last year of presidency. (That’s right, a Republican president for everyone out there under the impression this was the will of some Democratic socialist).

The Act, which was passed with bipartisan support by Congress, promised to ease the burden of repayment of student loan debt through a number of modifications to existing programs and the implementation of new programs, including PSLF, which was designed to forgive the remaining balance of a person’s federal student loans after they had made 120 qualifying payments while working in public service (e.g., a nonprofit gig).

Sounds awesome, right? Totally. Unfortunately, like most well-intended government programs, the PSLF Program had a ridiculous qualification structure and, in the 10 years after its inception, nearly 99% of applicants were denied.

In 2017, both Congress and the U.S. Department of Education attempted to remedy the situation and provide options for some rejected borrowers which still proved to be unproductive as they only allowed a certain amount to be forgiven for a specific number of people. In other words, a lot of red tape which continued to prove confusing and inaccessible for borrowers. Dumb.

Flash forward to 2021 and the PSLF temporary waiver, which was purposefully designed to eliminate all the bureaucratic madness and allow public service workers to have their federal student loans forgiven after 10 years of repayment, regardless of their loan program or repayment plan.

PSLF Waiver Applications

Again, for the people in the back, ONLY 15 PERCENT OF THE NINE MILLION PUBLIC SERVICE WORKERS WITH STUDENT LOAN DEBT HAVE FILED PAPERWORK TRACKING THEIR QUALIFYING PAYMENTS TOWARD PSLF. Fifteen percent, yo! In the same vein, more than 175,000 borrowers have received a total of $10 billion in student debt forgiveness under this new waiver, which is a good thing, but it doesn’t last for much longer. The temporary waiver expires at the end of October, which means you must act now!

If you are employed by a U.S. federal, state, local, or tribal government or not-for-profit organization – a classification that applies to teachers, nurses, veterans, government employees, and countless others who could work on behalf of for-profit organizations for far more money but don’t – you might be eligible for the PSLF Program. To determine whether you qualify, click here.

If you do in fact qualify, your next step is to complete the PSLF Form, which will require you to provide verification via your Human Resources department regarding your employment history. After the form is completed, simply send it to your loan service provider or to MOHELA, a federal loan service provider that administers the PSLF Program on behalf of the Department of Education.

If your PSLF form is approved for forgiveness, you will be notified that the entire remaining balance of your eligible student loan will be forgiven, including all outstanding interest and the principal balance. What’s more, if you made payments after your 120th qualifying payment, those payments will be treated as overpayments and be refunded to you as well. And yes, seriously, this is a real thing.

My Story

Once upon a time, I earned three academic degrees from two esteemed higher education institutions. My first was a bachelor’s degree in magazine journalism from Ball State University; the second was a paralegal certification from Capital University Law School; and the third was a master’s degree in journalism (again) from Ball State.

From 18 to 24 I worked my ass off academically and borrowed approximately $40,000 to supplement my education (a completely reasonable age-range to be given thousands of dollars in loans that would never, under any other circumstance, be granted otherwise, right?). I never changed my path or my major, and I always worked part-time.

After graduate school, I was employed by a for-profit company for a number of years before taking a job at a nonprofit institution that would not be surprised in the least by the profanity I use in this blog. I’ve worked for my current employer, in roles I truly love, for 10 years. Roles, I should mention, that REQUIRE the level of education I have achieved.

At 18, I had absolutely no idea what I was getting myself into in terms of loan repayment. I thought, ‘I’ll be able to pay them off later’ and, ‘this shouldn’t be a problem’ and also, ‘people do this all the time, right?’ The answers to these questions are no, no, and yes. Because after 16 years after earning my last degree, my student loans somehow skyrocketed to $55,000 and have gone down very little as I continued to pay on them regularly.

In all fairness, as a writer, math has never made much sense to me. However, seeing as how I’ve paid off other debts in my lifetime (including the credit card debt I also incurred at age 18), my student loan debt has never quite added up. How, after paying on my loans for nearly 20 years, has the amount increased by $15,000 with an estimated payoff date of January 2035? That’s 13 years from now and, god willing, my 10-year-old will have also graduated from college by then, too. Huh?

A few years ago I learned about the PSLF Program and attempted to determine how many of my payments qualified. At the time, even after working for a qualifying nonprofit for several years, none of my previous payments met the qualifications. Not one. For me, it was due to my repayment plan, which, if I changed it to meet the former PSLF standards, would have amounted to nearly double my mortgage each month.

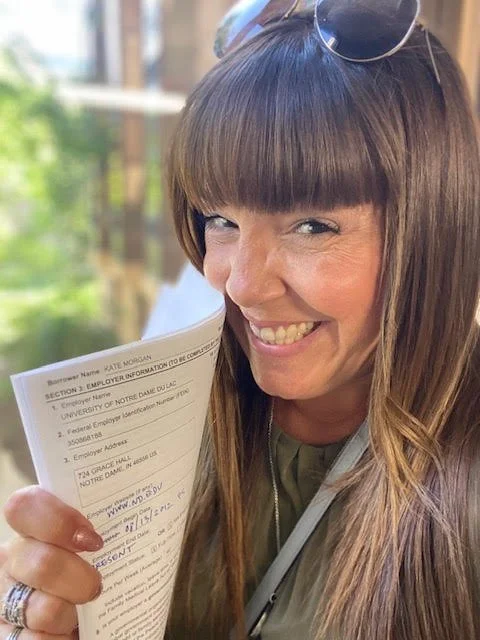

The day I submitted my final paperwork to receive PSLF loan forgiveness.